So far, we have constructed dependence using linear transformations of normal variables. This approach is powerful, but it has an important limitation:

It ties dependence to normality.

In many real-world applications (finance, insurance, environmental modelling), dependence can be:

non-linear,

asymmetric,

or stronger in extremes (tail dependence).

To model such behaviour, we need a more flexible framework.

This leads to the idea of copulas.

24.1 Copula

A copula is a function that allows us to construct a joint distribution by combining:

marginal distributions, and

a dependence structure.

Key Idea

Any joint distribution can be decomposed as:

\[

F_{X,Y}(x,y) = C\big(F_X(x), F_Y(y)\big),

\]

where:

\(F_X, F_Y\) are marginal CDFs,

\(C(u,v)\) is a copula.

This result is known as Sklar’s Theorem.

Interpretation

Marginals describe individual behaviour.

The copula describes dependence.

In copula models, dependence is often measured using:

Pearson correlation (linear)

Spearman’s rho (rank-based)

Kendall’s tau

Copulas naturally capture rank dependence, not just linear relationships.

Why Copulas Matter in Simulation

Copulas allow us to:

simulate dependence without assuming normality,

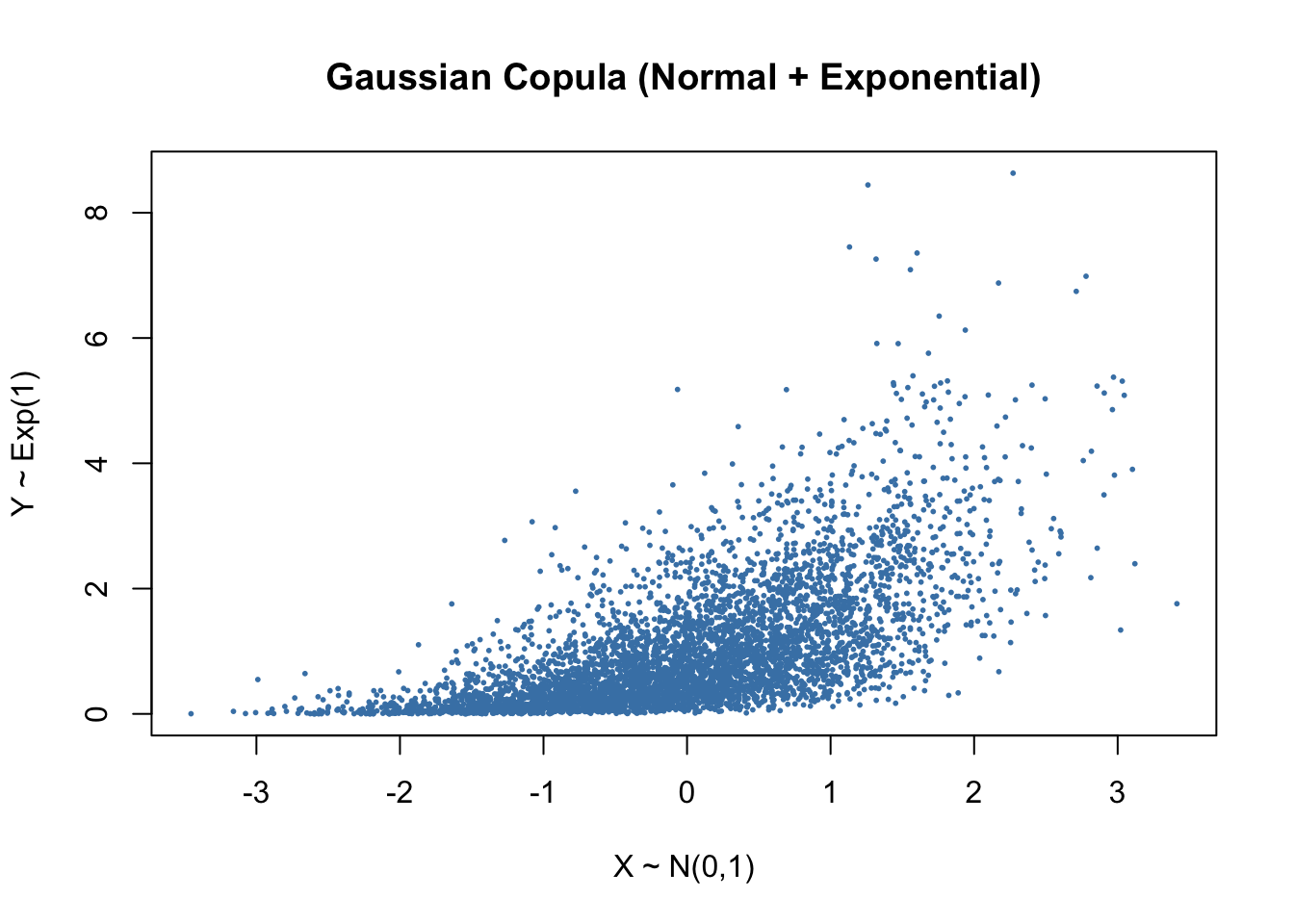

combine any marginal distributions (e.g., Normal + Exponential),

model tail dependence (important in risk modelling),

separate modelling into marginals (easy) or dependence (flexible).

Gaussian Copula

The most commonly used copula in simulation is the Gaussian copula.