So far, we have described temporal dependence visually and intuitively: some processes show persistence, some oscillate, and some behave almost like white noise. To measure this dependence more systematically, we use the autocorrelation function, or ACF.

The ACF is a general tool used to measure temporal dependence in any time series. We first study it in the context of AR(1), where it has a particularly simple form.

The ACF measures the correlation between a time series and a lagged version of itself.

For a time series \(X_t\), the lag-\(k\) autocorrelation is

\[

\rho_k = \text{Corr}(X_t, X_{t-k}).

\]

Here, \(k\) is called the lag.

For example:

lag 1 measures dependence between \(X_t\) and \(X_{t-1}\),

lag 2 measures dependence between \(X_t\) and \(X_{t-2}\),

lag 3 measures dependence between \(X_t\) and \(X_{t-3}\).

The ACF tells us how strongly the past is connected to the present.

If autocorrelations are close to zero, the process has little memory.

If autocorrelations decay slowly, shocks persist for a long time.

If autocorrelations alternate between positive and negative values, the process oscillates.

For white noise,

\[

\rho_k = 0 \quad \text{for all } k > 0,

\]

because observations at different times are independent.

For a stationary AR(1) process,

\[

X_t = \phi X_{t-1} + \varepsilon_t,

\]

the theoretical ACF is

\[

\rho_k = \phi^k.

\]

This is the same geometric decay pattern we observed in shock propagation.

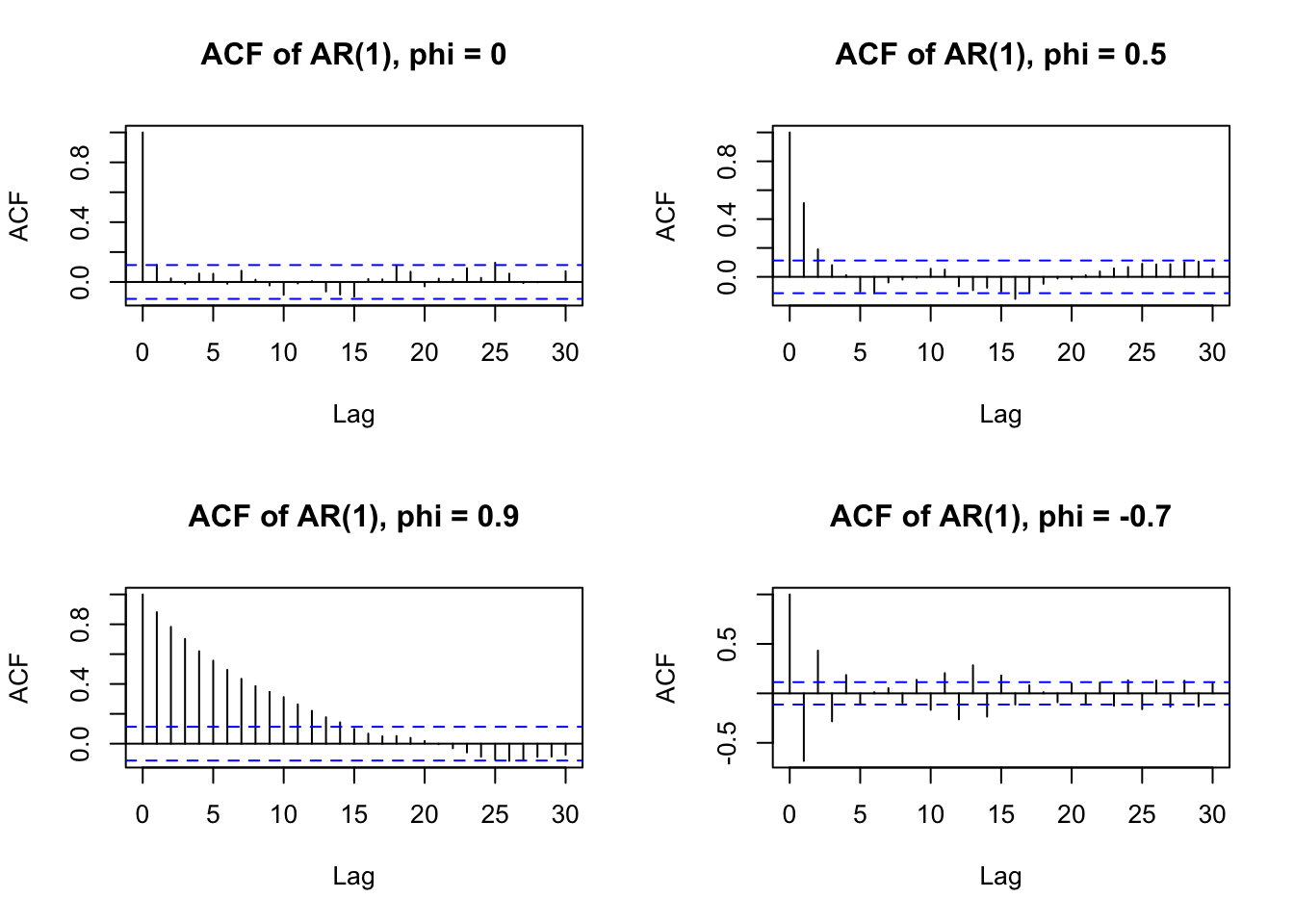

The value of \(\phi\) also determines the shape of the ACF:

Value of \(\phi\)

ACF behaviour

Interpretation

\(\phi = 0\)

zero after lag 0

white noise

\(0 < \phi < 1\)

positive decay

persistence

\(\phi \approx 1\)

slow decay

long memory

\(\phi < 0\)

alternating signs

oscillation

Thus, the ACF provides a numerical and visual way to diagnose temporal dependence.

Example: Compare the ACF of AR(1) processes with different values of \(\phi\).

set.seed(1234)n <-300phis <-c(0, 0.5, 0.9, -0.7)simulate_ar1 <-function(phi, n) { epsilon <-rnorm(n, mean =0, sd =1) X <-numeric(n) X[1] <-0for (t in2:n) { X[t] <- phi * X[t -1] + epsilon[t] }return(X)}par(mfrow =c(2, 2))for (phi in phis) { X <-simulate_ar1(phi, n)acf( X,main =paste("ACF of AR(1), phi =", phi),lag.max =30 )}