So far, the AR(1) model has described how a single variable depends on its own past:

\[

X_t = \phi X_{t-1} + \varepsilon_t.

\]

This captures memory within one time series. However, many real-world systems involve several variables that evolve together. In such systems, the future value of one variable may depend not only on its own past, but also on the past values of other variables.

For example:

energy demand may depend on past temperature,

stock returns may depend on past interest rates,

infection levels may depend on past mobility patterns,

queue length may depend on past arrival rates and service rates.

To model this kind of interaction, we extend AR(1) to a vector autoregressive model, or VAR.

shocks to one variable can influence the other variable later,

the two series move as an interacting system rather than as isolated processes.

This is the main conceptual leap from AR(1) to VAR.

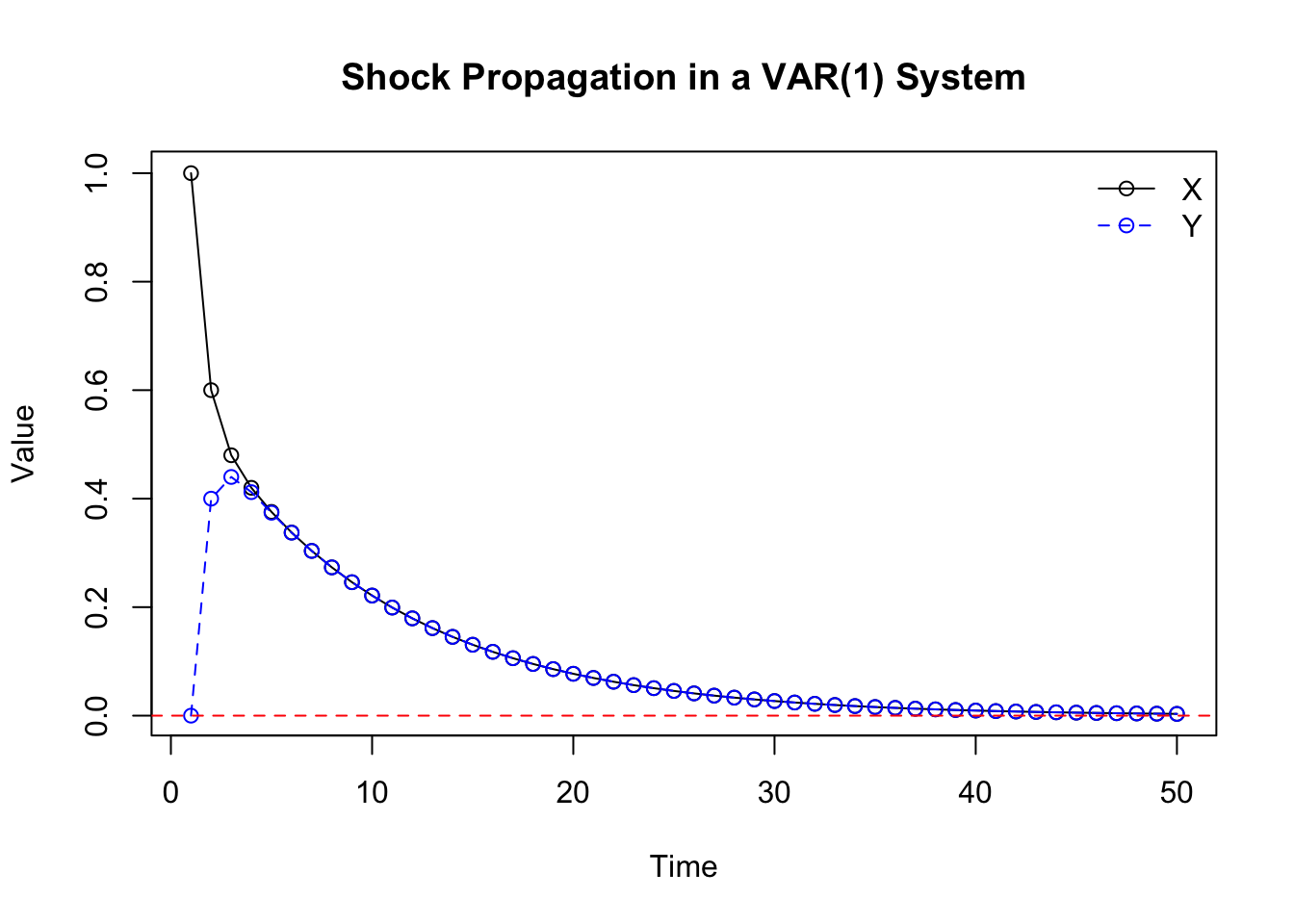

Isolating a Shock

To see cross-variable shock propagation more clearly, we can remove random noise and introduce a one-time shock to \(X\).

Example: A one-time shock to \(X\) propagates through both \(X\) and \(Y\).

n <-50X <-numeric(n)Y <-numeric(n)X[1] <-1# initial shock to XY[1] <-0for (t in2:n) { X[t] <-0.6* X[t -1] +0.3* Y[t -1] Y[t] <-0.4* X[t -1] +0.5* Y[t -1]}plot( X,type ="o",main ="Shock Propagation in a VAR(1) System",xlab ="Time",ylab ="Value")lines(Y, type ="o", lty =2, col ="blue")abline(h =0, col ="red", lty =2)legend("topright",legend =c("X", "Y"),lty =c(1, 2),pch =c(1, 1),col =c("black", "blue"),bty ="n")

Python Version

import numpy as npimport matplotlib.pyplot as pltn =50X = np.zeros(n)Y = np.zeros(n)X[0] =1# initial shock to XY[0] =0for t inrange(1, n): X[t] =0.6* X[t -1] +0.3* Y[t -1] Y[t] =0.4* X[t -1] +0.5* Y[t -1]plt.plot(X, marker="o", label="X")plt.plot(Y, marker="o", linestyle="--", label="Y")plt.axhline(0, color="red", linestyle="--")plt.title("Shock Propagation in a VAR(1) System")plt.xlabel("Time")plt.ylabel("Value")plt.legend()plt.show()

The plot shows that the initial shock directly affects \(X\), but then spreads to \(Y\) through the cross-effect term \(a_{21}\). Once \(Y\) changes, it can also feed back into \(X\) through \(a_{12}\).

Thus, a VAR model allows us to study not only whether shocks persist, but also where they travel.

Comparison: AR(1) vs VAR(1)

Feature

AR(1)

VAR(1)

Number of variables

One

Two or more

Dependence

Own past only

Own past and other variables’ past

Shock propagation

Through time

Through time and across variables

Main idea

Memory

Interaction

VAR extends the AR idea from a single time series to an interacting system of time series.

The same ideas remain central:

memory,

persistence,

shock propagation,

stability,

simulation.

The only difference is that shocks can now move between variables, not just through time within one variable.